Tokyo—Japan’s smartphone market roared back in 2025, but the deals that made it famous may be nearing a turning point. MM Research Institute (MMRI) reported that domestic mobile phone shipments climbed for a second straight year, even as a looming spike in global memory prices threatens to push up handset costs in 2026—potentially ending Japan’s hallmark “¥1 phone” offers.

Key findings from MMRI’s 2025 report

Shipments and 5G dominance

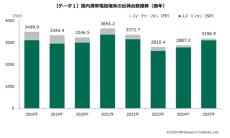

MMRI’s latest data shows total smartphone shipments in Japan reached 31.114 million units in 2025, up 11.6% year on year. Feature phones fell to just 0.855 million units, down 12.6%, as the smartphone share of the overall market rose to 97.3%. The 5G transition is now essentially complete: 5G devices totaled 30.946 million units, up 11.5% and representing 99.5% of all smartphones shipped. MMRI attributes the growth to stable replacement demand fueled by carriers’ buyback and return-at-upgrade programs—plans that lower the effective monthly cost when customers agree to return handsets after one or two years—combined with intense competition among operators. The countdown to NTT Docomo’s scheduled 3G shutdown by March 2026 also nudged remaining legacy users to upgrade, pushing feature-phone volumes to a new low.

Who won in 2025: Apple leads, Google second

Apple reclaimed scale in Japan, shipping 15.782 million units (+12.1% y/y) and taking a 49.4% share of total mobile shipments. On smartphones alone, Apple’s share hit 50.7%, marking three consecutive years above the 50% line. Google ranked second with 3.854 million units (12.1% share), followed by Samsung at 3.433 million (10.7%). Domestic champions remained central to the market’s fabric: Sharp placed fourth with 2.497 million (7.8%), FCNT fifth at 2.054 million (6.4%), and Kyocera sixth with 1.237 million (3.9%). Together, the top six controlled 90.3% of shipments—evidence of a highly competitive yet well-defined landscape.

Pricing shifts: Android widens the entry ramp

Japan’s price mix continued to bifurcate in 2025. The sub-¥29,999 (tax-in) entry segment expanded from 3.8% in 2019 to 14.4% in 2025. All models in that bracket were Android, reflecting manufacturers’ success at meeting value-focused demand within Japan’s regulatory guardrails. On iPhone, entry-tier devices were absent; approximately 96% of Apple’s 2025 shipments were priced at ¥100,000 and above, reinforcing its premium positioning. Android stretched both ends of the spectrum: its sub-¥29,999 share jumped from 7.3% in 2019 to 29.1% in 2025 (about four times higher), while its ¥100,000-plus segment also grew to 18.2%. The rise of budget Androids aligns with amendments to Japan’s Telecommunications Business Act, which capped carrier discounts (commonly up to around ¥22,000). That ceiling incentivized OEMs and carriers to design compelling entry models that, once the legal discount is applied, could be marketed for “¥1” on certain plans with trade-in or return conditions.

Why “¥1 phones” may fade in 2026

AI boom fuels memory cost surge

While 2025 was buoyant, MMRI warns that the global AI boom is driving rapid price increases for memory components—DRAM, NAND, and SSD—since late 2025. Because memory is a large share of a smartphone’s bill of materials, a sustained component rally in 2026 would push up retail pricing. MMRI highlights a critical question: can low-cost Android models that currently hit ¥1 after applying the roughly ¥22,000 legal discount still be manufactured at viable unit costs? If not, carriers may be forced to scale back or end “¥1” promotions, which could, in turn, dampen overall shipments.

Implications for consumers, carriers, and makers

For consumers in Japan—including expats and long-stay visitors—the end of ultra-cheap entry deals would shift value toward midrange models on installment, SIM-only plans, and certified refurbished units. Carriers may lean more heavily on return-at-upgrade programs and data bundle differentiation as device subsidies lose punch. For manufacturers, Japan’s market remains attractive: premium segments are healthy (especially for Apple), while Android’s breadth offers room to innovate at both the entry and high end. However, balancing memory configurations, AI-capable chipsets, and price-sensitive SKUs will become more challenging if component inflation persists.

Why this matters to foreign residents and Japan-watchers

Japan’s mobile ecosystem is one of the world’s most advanced: 5G is near-universal in new shipments, customer service is rigorous, and competition among carriers keeps experiences and networks strong. Regulation has nudged the market toward transparency and broader affordability, helping newcomers access reliable connectivity from day one. If the “¥1 phone” era recedes in 2026, expect Japan to adapt quickly—through competitive MVNO options, installment flexibility, and robust trade-in ecosystems. The net effect should keep Japan an easy, high-quality place to get connected—even as global supply cycles test pricing. In short, 2025 underscores Japan’s resilience and dynamism; 2026 will test its ingenuity.