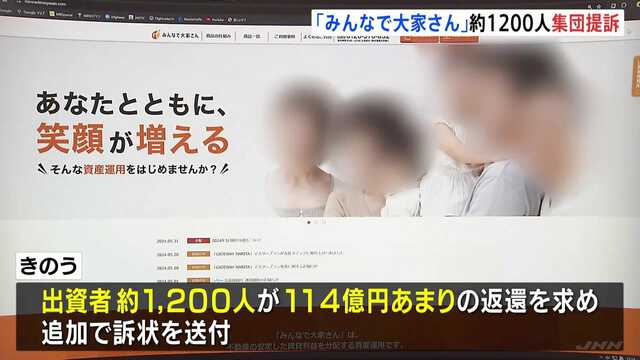

About 1,200 investors have filed a mass claim against “Minna de Ooyasan,” a popular Japanese real estate investment product whose delayed payouts have alarmed tens of thousands of retail customers. The group is seeking the return of more than ¥11.4 billion—roughly $75 million at recent exchange rates—submitting their complaint to the Osaka District Court on the 5th, according to lawyers representing the plaintiffs. The move escalates a legal campaign that began in September, when five investors first brought a case over halted distributions.

What is “Minna de Ooyasan”?

“Minna de Ooyasan” (literally, “Let’s all be landlords”) is a real estate investment product marketed to individual investors in Japan. It has pitched annual distributions of around 7%, attracting more than 37,000 people and collecting in excess of ¥200 billion (approximately $1.3 billion). The offering drew interest in a market long characterized by ultra-low yields, appealing to savers seeking steady income backed by real assets. Investors typically participate via product units tied to specific projects, with distributions funded by rents or development proceeds. Although often described colloquially as a fund, the products can vary in structure, and the exact legal mechanics determine investor protections, disclosure obligations, and recourse in the event of distress.

The Flashpoint: Gateway Narita and Widespread Payout Suspensions

Trouble sharpened this summer around “Gateway Narita,” a flagship urban development project near Narita Airport meant to anchor part of the “Minna de Ooyasan” portfolio. According to investor communications cited by plaintiffs, distributions have not been paid since July for this project. More broadly, payouts have reportedly stopped for 33 of the program’s 35 products, signaling a systemwide cash-flow squeeze. In Fukuoka Prefecture, one of the targeted assets includes a banana production facility in the Kitakyushu area—unusual as a real estate play but packaged within the broader investment lineup—which has also experienced delayed distributions. The breadth of non-payment has rattled participants who had come to rely on the promised 7% annual income.

A Legal Campaign Gathers Pace

The plaintiffs’ attorneys say five investors filed an initial lawsuit in September. On the 5th, about 1,200 additional participants from Fukuoka and other regions submitted their complaint to the Osaka District Court, seeking restitution of principal and other sums. The latest filing concentrates on recovering funds rather than forcing resumed distributions, a stance that suggests investors increasingly doubt the near-term viability of the projects’ cash flows. As of publication, the operator behind “Minna de Ooyasan” had not publicly responded to the collective lawsuit. The court will likely review standing, consolidate related claims, and set an initial hearing schedule in the coming weeks or months.

Why the Payouts Stopped: What We Know—and Don’t

While the company has not offered a comprehensive public explanation, the pattern of suspensions points to multiple pressure points. Development-heavy portfolios are vulnerable to construction delays, cost inflation, and financing challenges. Japan’s building materials and labor costs have climbed in recent years, squeezing margins. Higher global interest rates have tightened funding conditions even in Japan’s low-rate environment, particularly for borrowers reliant on rollover financing or project-specific debt. Projects near major transport hubs like Narita Airport can also face complex zoning, infrastructure, and permitting hurdles that, if prolonged, disrupt expected timelines for rent generation or sales proceeds. In agriculture-adjacent assets, such as the Kitakyushu banana facility, operational risks—crop yields, supply chain consistency, and market pricing—may add volatility not typical of standard commercial property. None of these factors, on their own, prove mismanagement or misconduct. But in combination they can create a cash-flow crunch that translates directly into missed distributions. The high headline yield of 7% is another clue: in benign markets, such payouts can be sustained, but under stress they often prove aspirational, contingent on smooth execution and steady financing.

Retail Investors in the Crosshairs

Japan’s prolonged low-interest-rate era pushed households toward alternative income products, including real estate-linked offerings and crowdfunding-style platforms. Many investors accepted illiquidity and project risk in exchange for yield. The “Minna de Ooyasan” case underscores how those trade-offs can crystallize: when distributions falter, investors’ ability to exit or recover principal may depend on legal rights embedded in contracts and on the operator’s transparency. Market observers say the episode could become a litmus test for how Japan protects retail investors in complex property vehicles, a sector that has grown faster than public familiarity with its risks.

What Happens Next

Several scenarios are possible. If the operator can stabilize cash flows—through asset sales, refinancing, or restructuring of development timelines—some distributions could resume, potentially at reduced rates. Alternatively, the company might propose a restructuring plan, exchanging near-term payouts for longer maturities or contingent returns tied to project milestones. Court-mediated settlements could clarify the order of repayment and the status of investors vis-à-vis other creditors. For the plaintiffs, the priority is restitution: the claim of more than ¥11.4 billion suggests a focus on capital recovery rather than waiting indefinitely for distributions to restart.

Regulatory and Market Implications

Japanese authorities have encouraged clearer investor disclosures in recent years, but the proliferation of non-traditional real estate products has outpaced uniform standards in how risks are communicated. A high-profile court case may prompt tighter guidance on marketing language around “target” yields and liquidity, as well as more robust monitoring of project-level performance. For the broader market, the episode could cool retail appetite for yield-focused property products, at least until operators demonstrate more resilient funding structures and contingency planning.

Company Silence and Investor Patience

The “Minna de Ooyasan” operator has not, as yet, commented on the latest collective filing. In the absence of detailed explanations, investors face a difficult wait: asset-heavy portfolios take time to monetize, and development timelines rarely move quickly once delayed. For now, the legal process offers one avenue of recourse, while the market gauges whether this is an isolated crisis of execution or a warning sign for similarly structured offerings. Either way, the case has become a watershed moment for Japan’s retail real estate investment landscape—highlighting the perils of chasing yield without a full understanding of how that income is generated and what happens when the cash stops flowing.